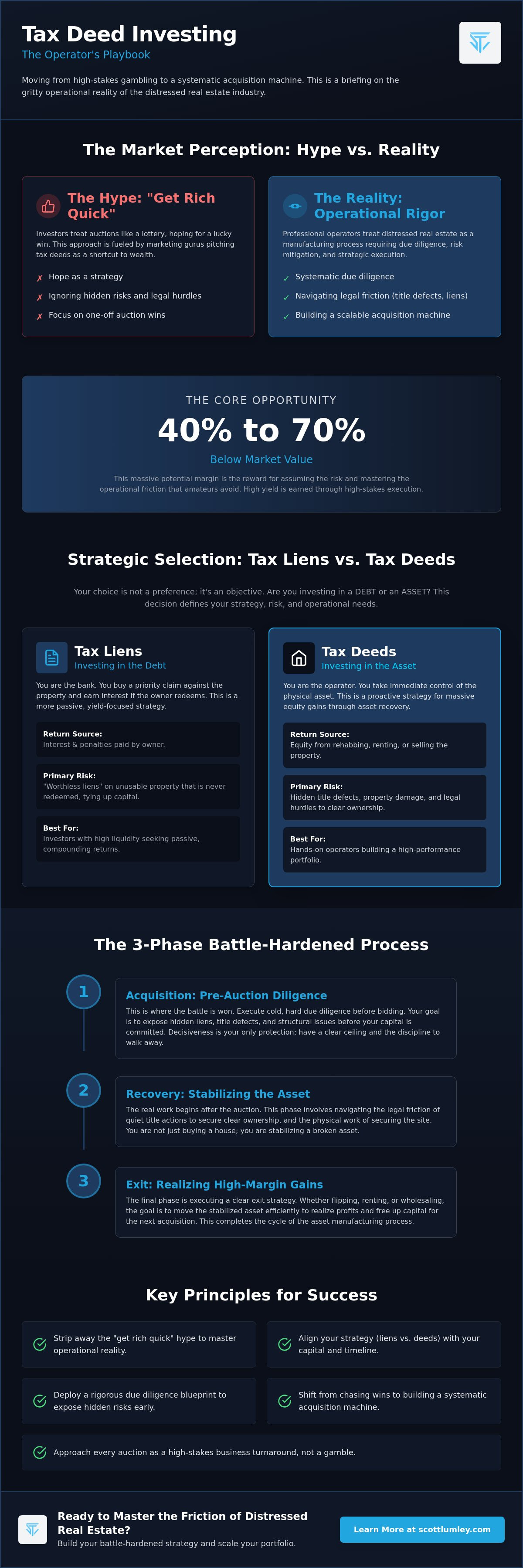

Most investors treat the tax deed auction like a high-stakes lottery, but hope is not a strategy when your capital is on the line. If you want to survive in this game, you need a tax deed investing strategy built on operational rigor rather than luck. The reality of distressed real estate is messy. It's full of hidden liens, title defects, and shifting state laws that can bury an amateur in weeks. You've likely felt the frustration of trying to turn a single auction win into a predictable business model.

We agree that the potential for high-margin assets is massive, with properties often selling for 40% to 70% below market value. However, the fear of a catastrophic title issue is a legitimate barrier to scaling. This article promises to move you past the theory and into a repeatable due diligence system that mitigates risk at every turn. We won't waste time on motivational fluff or optimistic theories.

Instead, we'll dive into the mechanics of asset acquisition, the impact of evolving tax legislation, and the specific steps required to clear titles. This is a briefing on the gritty operational reality of the industry, providing a clear path to portfolio expansion through a battle-hardened approach to the market.

Key Takeaways

- Strip away the "get rich quick" hype to master the operational reality of acquiring assets through government foreclosures.

- Learn to evaluate the risk profiles of tax liens versus deeds to ensure your tax deed investing strategy aligns with your capital liquidity and timeline.

- Deploy a rigorous due diligence blueprint that exposes hidden liens and structural issues before they compromise your portfolio.

- Shift from chasing one-off auction wins to building a systematic acquisition machine capable of managing a geographically diverse asset base.

- Approach every auction as a high-stakes business turnaround rather than a gamble, focusing on recovery and strategic execution.

The Reality of Tax Deed Investing: Beyond the "Get Rich Quick" Hype

A tax deed isn't a discount coupon for a dream home. It's a legal instrument representing the transfer of property ownership following a government foreclosure for delinquent taxes. While marketing "gurus" pitch this as a shortcut to wealth, the reality is a high-friction environment of asset recovery and legal hurdles. If you approach this without a battle-hardened tax deed investing strategy, you aren't an investor; you're a gambler. Success in the tax sale process requires moving past the hype and focusing on the operational reality of distressed real estate.

Winning at an auction is the easy part. The real work begins when the gavel drops and you inherit the problems the previous owner couldn't solve. For growth-oriented portfolios, tax deeds represent a powerful asset class, but they demand a level of strategic execution that most retail investors aren't prepared to provide. You're not just buying land; you're buying a legal situation that requires resolution.

High Yield vs. High Stakes: The Real Trade-off

Tax deeds offer deep discounts because the buyer assumes all the risk. These properties are sold "as-is" and "where-is" without the protections of a traditional real estate transaction. You can't walk through the front door or inspect the plumbing before your capital is committed. You might buy a pristine rental or a pile of rubble; the auction doesn't care. The redemption period is the legal window during which the former owner can reclaim the property by paying off the debt, interest, and penalties, which can freeze your capital and delay your ROI.

The Battle-Hardened Investor Mindset

Passive investors get crushed in this market. They treat auctions like a hobby, hoping for a bargain without understanding the recovery phase. Professional operators treat distressed real estate as a manufacturing process involving acquisition, recovery, and exit. You're not just buying a house; you're stabilizing a broken asset.

- Acquisition: Executing cold, hard due diligence before the bidding starts.

- Recovery: Navigating the legal friction of quiet title actions and the physical securing of the site.

- Exit: Moving the asset quickly to realize high-margin gains.

In the bidding room, decisiveness is your only protection. You must have a clear ceiling and the discipline to walk away when the price exceeds your strategy's limits. A winning bid becomes a liability the moment the math stops accounting for the friction of the recovery process. Don't let the adrenaline of the auction room override the reality of your balance sheet.

Strategic Selection: Tax Liens vs. Tax Deeds

Choosing between a tax lien and a tax deed isn't a matter of preference. It's a matter of objective. You are either investing in a debt or an asset. One is a passive play for interest; the other is a proactive play for equity. Your choice determines the level of friction you'll face and the operational infrastructure you'll need to build. Aligning your choice with your broader financial goals is the first step in moving from an amateur bidder to a professional operator.

Investing in the Debt: The Tax Lien Strategy

Tax liens are for those who want to play the role of the bank. When you purchase a lien, you aren't buying the property. You're buying a priority claim against it. Your return comes from the interest and penalties paid by the owner to redeem the property. If they pay, you collect a check. If they don't, you eventually gain the right to foreclose, though this happens in less than 2% of cases nationally.

The danger here is the "worthless lien." Institutional investors often dominate this space, using high-volume algorithms to sweep up certificates. If you aren't careful, you'll end up holding a lien on a toxic waste site, a condemned slum, or a strip of unusable land. In these scenarios, the owner won't redeem, and you won't want to foreclose. Your capital is effectively dead. This is a growth play for those with high liquidity who can afford to wait for compounding interest.

Investing in the Asset: The Tax Deed Strategy

Deeds are different. This is the core of a high-performance tax deed investing strategy. You aren't waiting for a check in the mail; you're taking immediate control of the asset. When the gavel falls, you own the dirt and everything on it. This path offers the potential for massive equity gains, often acquiring properties for a fraction of their market value. However, it requires a "boots on the ground" approach that liens do not.

You must verify the physical condition and the legal status of every asset. For a comprehensive guide to tax deed investing, you'll find that the hurdle isn't just the auction; it's the title curative work required to make the property salable. This is a turnaround objective. You find a broken situation, deploy your system to fix it, and exit with a profit. It's gritty, it's labor-intensive, and it's where the real money is made. If you need a sounding board for your next move, professional Real Estate Advisory can help refine your acquisition criteria before you commit capital.

Whether you choose the debt or the asset depends on your appetite for friction. Liens offer a cleaner, slower path. Deeds offer a faster, more aggressive route to portfolio expansion. Both require a level of due diligence that most investors simply won't perform. Don't be "most investors."

The Due Diligence Blueprint: Stripping Away Operational Friction

Due diligence isn't "homework." It's a survival mechanism. In the world of distressed real estate, the most profitable move you'll ever make is the bid you decide not to place. A professional tax deed investing strategy relies on a cold, clinical assessment of risk before a single dollar is committed. Amateurs chase the potential upside of a cheap property; professionals hunt for the friction points that will bleed their margins dry. If you can't identify the exit path before the auction, you shouldn't be in the room.

Your blueprint must be a "no-nonsense" filter designed to kill bad deals quickly. This isn't about finding reasons to buy. It's about finding reasons to walk away. Every asset you evaluate should be subjected to a rigorous checklist:

- Superior Lien Verification: Identify debts that survive the foreclosure.

- Zoning and Land Use: Ensure the dirt is actually buildable or usable.

- Environmental Hazards: Check for underground tanks or soil contamination.

- Occupancy Status: Determine if you're buying an empty shell or a legal battle with a holdover owner.

By treating this as an operational turnaround, you stop viewing properties as "deals" and start seeing them as projects. This mindset shift allows you to price in the friction of asset recovery from the start. If the numbers don't work with a 20% contingency for the unknown, the deal is dead.

The Title Search: Identifying Superior Liens

The biggest myth in this industry is that a tax deed wipes out every other debt. It doesn't. While many junior liens are extinguished, superior liens like IRS tax liens or certain municipal assessments can remain attached to the property. If you miss these, you're effectively paying the previous owner's debt on top of your bid price. Clouded titles can freeze your capital for years, preventing you from selling or even getting a construction loan. A Quiet Title Action is a mandatory legal proceeding required to clear these title defects and ensure the property can be sold or refinanced with title insurance. According to 2026 industry data, the average cost for a quiet title action ranges between $1,500 and $5,000, a cost that must be baked into your initial bid.

Physical Inspection and Occupancy Challenges

Buying sight-unseen is a gamble, not an investment. Even if you can't get inside, a physical "drive-by" inspection is non-negotiable. You need to know if the structure is standing or if it's been stripped of its copper and HVAC systems. Beyond the physical, you must account for the human element. Dealing with squatters or former owners who refuse to leave is the gritty reality of asset recovery. This process requires a steady hand and a clear legal strategy for eviction or cash-for-keys. Always build a stabilization fund into your bid price to cover immediate costs like boarding up windows, changing locks, or basic site cleanup. This is how you mitigate the risk of catastrophic structural disasters and ensure your tax deed investing strategy remains scalable.

Operationalizing Your Tax Deed Strategy for Growth

Scaling isn't about bidding on more houses. It's about building a machine that finds, vets, and recovers assets without your constant intervention. Most investors get stuck in the "one-off" trap. They win an auction, struggle through the recovery, and then start from zero again. This is a hobby, not a business. A professional tax deed investing strategy demands a systematic approach to portfolio expansion. You need a structure that supports a geographically diverse asset base while maintaining the same level of due diligence rigor across every county line.

Leveraging a Property Tax Debt System allows you to automate the identification of distressed opportunities. Instead of manually scouring county records, you deploy technology to flag assets that meet your specific risk profile. This is where Strategic Planning becomes your most valuable tool. You aren't just reacting to what's available; you're targeting specific markets based on recovery timelines and exit demand.

Building the Operational Infrastructure

You can't scale from your kitchen table. A systematic portfolio requires a team of local inspectors, title attorneys, and property managers who understand the friction of tax deeds. You need boots on the ground in every jurisdiction where you bid. Technology serves as the backbone, providing rapid due diligence at scale. However, the biggest bottleneck to growth is cash flow. You must manage your capital through the waiting period of title clearing. If your liquidity is tied up in a three-year redemption window without a plan, your growth engine stalls.

Strategic Exit Planning: Flip, Rent, or Hold?

The exit strategy is decided before the bid is placed. You must evaluate the asset's highest and best use while it's still on the auction block. Are you flipping for immediate capital recycling? Are you holding for long-term equity growth? Applying business growth principles means maximizing the equity in every acquired deed through efficient stabilization. This requires a clear-eyed assessment of the market and the asset's physical condition.

If the property requires significant rehab, you need specialized leadership in construction to manage the recovery phase. This isn't just about painting walls; it's about asset stabilization. Once the title is clear and the asset is recovered, you move fast. Recycling capital is the only way to keep the growth engine moving. If you're looking to professionalize your operation, Leadership Consulting can provide the framework for managing a high-stakes real estate team and a scaling portfolio.

Navigating the Recovery Zone: Why Strategy Beats Luck

Luck is a poor substitute for a system. In the high-stakes environment of distressed real estate, banking on fortune is a quick way to lose your capital. You must view every auction win as a business turnaround opportunity. It's an operational play. A successful tax deed investing strategy isn't about being the highest bidder; it's about being the most prepared operator. The recovery zone is where the weak are filtered out and the professionals realize their margins.

This gritty approach is informed by Scott Lumley’s 40 years of experience in construction and logistics. Real estate isn't just about dirt. It's about moving assets through a pipeline of recovery and stabilization. When you treat a property like a logistical challenge, you identify friction points that others miss. You see the structural issues, the legal hurdles, and the exit barriers before the gavel falls. This level of insight only comes from decades spent in the trenches of high-stakes operations.

Amateur investors make fatal mistakes because they don't know what they don't know. They skip the deep dive. They ignore the superior liens. They underestimate the cost of stabilization. Engaging in professional Due Diligence consulting isn't an expense; it's an insurance policy against catastrophic loss. The winners in this market aren't those with the biggest checkbooks. They're the ones with the best systems. Strategy beats luck every single time.

Leadership in Distressed Real Estate

Moving from a tactical hunter to a strategic portfolio manager requires a shift in mindset. You can't just chase the next deal. You have to lead a firm. This is why specialized Real Estate Advisory is critical for those entering the space. You need a battle-hardened advisor who has navigated the complex operational storms you're about to face. A strategic leader focuses on the long-term health of the portfolio, balancing risk across multiple jurisdictions. They don't just survive the recovery zone; they dominate it.

The Property Tax Debt System

Sustainable growth isn't accidental. It's the result of a repeatable process. By utilizing a Property Tax Debt System, you create a deal-finding machine that operates with clinical precision. This moves you beyond the realm of theory and into the reality of strategic execution. You stop guessing and start executing. It's time to professionalize your approach and treat your investments like the high-stakes business they are. Scale your real estate leadership with Scott Lumley’s strategic advisory and build a portfolio that lasts.

Master the Friction of Distressed Real Estate

Tax deed investing isn't a passive sideline. It's a high-stakes operational business. You've seen that success depends on moving beyond the auction hype and into the gritty reality of asset recovery. A professional tax deed investing strategy requires a clinical due diligence blueprint and a systematic approach to scaling. Without these, you're just another amateur hoping for a bargain in a room full of professionals. You must treat every acquisition as a manufacturing process: acquire, stabilize, and exit.

Scott Lumley brings 40 years of hands-on operational experience to the table. His deep background in construction and logistics provides the rugged resilience needed to navigate complex real estate turnarounds. By utilizing his specialized Property Tax Debt System, you can transform one-off auction wins into a sustainable growth engine. Don't leave your capital to chance. It's time to build a deal-finding machine that minimizes friction and maximizes your equity gains. The path to a scalable portfolio is open to those willing to do the hard work of strategic execution.

Execute your high-stakes real estate strategy with Scott Lumley. Your next move starts here.

Frequently Asked Questions

Is tax deed investing safe for beginners?

No. It's a high-stakes operational play that punishingly filters out the unprepared. Beginners often lack the due diligence infrastructure to identify hidden liabilities like superior liens or environmental hazards. Without a battle-hardened system, you aren't investing; you're gambling with your capital in a room full of professionals.

What is the biggest risk in tax deed investing strategy?

The biggest risk is inheriting a liability that exceeds the property's value. Superior IRS liens, municipal assessments, or catastrophic structural defects don't always disappear at auction. A professional tax deed investing strategy focuses on killing these deals before the bidding starts. If you miss a title defect, there are no refunds at the county courthouse.

How much capital do I need to start a tax deed investment business?

You need enough liquidity to cover the bid price, immediate stabilization, and legal fees. Bidding with your last dollar is a recipe for failure. Beyond the auction price, you must budget for title curative work and property taxes that accrue during the recovery phase. Capital requirements vary by jurisdiction, but your budget must account for friction, not just the asset price.

Can I lose my entire investment in a tax deed sale?

Yes. Total loss occurs when you acquire an asset that is legally or physically unsalable. This happens when investors buy "sight-unseen" and discover a condemned structure or a property with massive environmental contamination. In this game, the government doesn't guarantee the condition or the title of what they're selling.

How does a tax deed differ from a tax lien in terms of ROI?

Liens offer interest-based returns; deeds offer equity-based returns. A tax lien is a passive play where you earn a check from interest and penalties. A tax deed investing strategy is an aggressive play for total control of the asset. You're trading the safety of a lien for the high-margin potential of owning the dirt at a deep discount.

What happens to the mortgage on a property bought at a tax deed sale?

In most jurisdictions, a tax deed sale wipes out junior liens, including the mortgage. This isn't a universal rule. You must verify local statutes and ensure all parties were properly notified of the foreclosure. If the county failed to notify the lender, the mortgage might survive the sale, turning your "bargain" into a financial disaster.

Do I need a lawyer for every tax deed purchase?

You need legal expertise for the recovery phase, specifically for title curative work. While you can bid without an attorney, you cannot sell the property or get title insurance without a quiet title action. Professional operators build these legal costs into their initial bid price to ensure the asset is salable on the back end.

How long does it take to get a clear title after a tax deed auction?

Expect a timeline of six months to a year. This window accounts for the mandatory legal proceedings of a quiet title action and any statutory redemption periods. It's an operational marathon. You must manage your cash flow through this waiting period to ensure your growth engine doesn't stall while the legal system clears your path.